Strong rebound in pending home sales

WASHINGTON – Dec. 2, 2010 – Pending home sales jumped 10.4 percent in October, showing another positive uptrend since bottoming in June, according to the National Association of Realtors®.

The Pending Home Sales Index (PHSI), a forward-looking indicator, rose to 89.3 based on contracts signed in October from 80.9 in September. The index remains 20.5 percent below a surge to a cyclical peak of 112.4 in October 2009, which was the highest level since May 2006 when it hit 112.6.

The latest surge also reflects market strength, since buyers had an additional push to close quickly in October 2009 to qualify for one version of the first-time homebuyer tax credit that expired in November. The data reflects contracts and not closings, which normally occur with a lag time of one or two months.

The data also surprised economists who had expected a decline in pending home sales given current troubles within the housing market. However, Lawrence Yun, NAR chief economist, says excellent housing affordability conditions drew in more homebuyers.

“It is welcoming to see a solid double-digit percentage gain, but activity needs to improve further to reach healthy, sustainable levels,” Yun says. “The housing market clearly is in a recovery phase and will be uneven at times, but the improving job market and consequential boost to household formation will help the recovery process going into 2011. More importantly, a return to more normal loan underwriting standards and removal of unnecessary underwriting fees for very low risk borrowers is needed and could quickly help in the housing and economic recovery.”

Recent loan performance data from Fannie Mae and Freddie Mac clearly demonstrates very low default rates on recently originated mortgages – much lower that the vintages of 2002 and 2003 before the housing boom.

The PHSI in the Northeast jumped 19.6 percent to 71.3 in October but is 27.3 percent below the tax credit peak in October 2009. In the Midwest, the index surged 27.3 percent in October to 81.7 but is 24.8 percent below a year ago.

Pending home sales in the South rose 7.1 percent to an index of 93.8 but are 18.4 percent below October 2009. In the West, the index slipped 0.4 percent to 104.3 and is 15.6 percent below a year ago.

Near term, Yun expects home sales to continue climbing from their cyclical low this past summer.

“Even so, we now have some consumer concerns regarding the mortgage interest deduction, an important component in housing affordability,” Yun says.

© 2010 Florida Realtors®

Wednesday, December 15, 2010

Monday, December 6, 2010

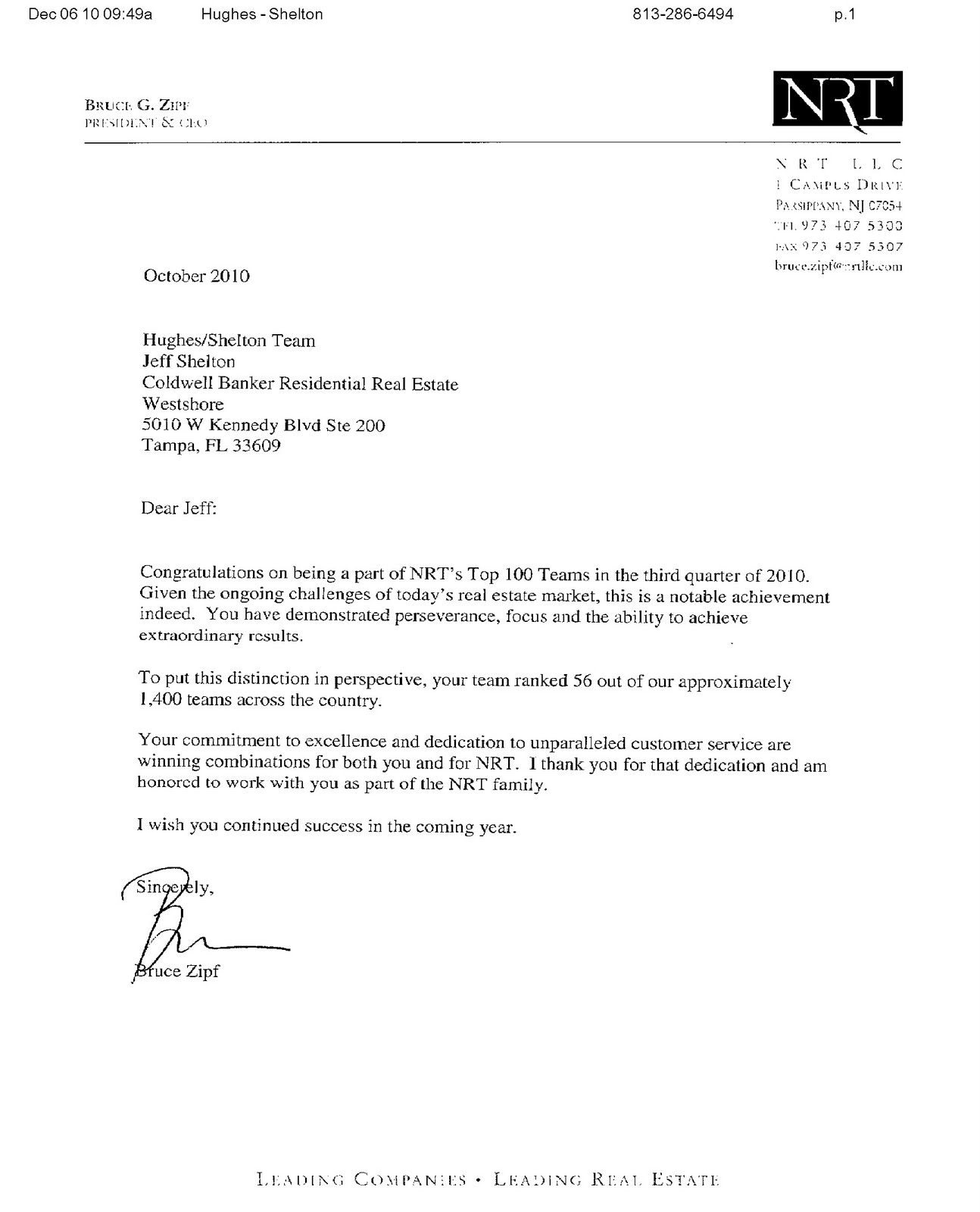

Hughes-Shelton Realtors in top 100 of Coldwell Banker Nationwide!

Hughes-Shelton Realtors is ranked #56 of all teams within Coldwell Banker nationwide!

Monday, November 29, 2010

Consumers Spend and Earn More

WASHINGTON (AP) – Nov. 24, 2010 – Americans earned more and spent more last month, and the number of people applying for unemployment benefits dropped last week to the lowest level in more than two years. At the same time, demand for long-lasting manufactured goods and new homes fell off.

All told, the latest government data released the day before Thanksgiving suggest an improving picture of the economy. Income and spending are rising, and layoffs are slowing. This comes amid a decline in manufacturing activity, which had been a source of strength for months after the recession ended, and a struggling housing market.

Analysts question whether incomes can continue to grow at a consistent pace and keep consumers spending enough to invigorate the economy.

“The flurry of U.S. data this morning suggests that households have started to pickup the baton of growth from businesses,” said Paul Dales, U.S. economist at Capital Economics. “Whether or not households will be able to shoulder the burden of growth on their own is another matter.”

Investors appeared to be pleased by the data. The Dow Jones industrial average climbed more than 137 points in the early morning trading.

Consumers boosted their spending 0.4 percent in October, the Commerce Department said Wednesday. That was up from a 0.3 percent increase in September.

People showed a slightly bigger appetite to spend because their incomes rose 0.5 percent, reflecting a slowly healing jobs market that gave a boost to wages and salaries. Incomes didn’t grow at all in September. The increases in both income and spending last month were the most since August.

And inflation is running lower at a record low. Prices for goods excluding food and energy rose just 0.9 percent in the 12 months ending in October, the Commerce report noted. That was down from a 1.2 percent annual gain posted in September. Inflation is running at a pace below the Fed’s comfort zone of between 1.5 percent and 2 percent.

“We have a good signal,” John Silvia, chief economist at Wells Fargo, said of the jobless claims and consumer spending reports.

The pace of layoffs slowed to the lowest level since July 2008. Initial jobless claims dropped by 34,000 to a seasonally adjusted 407,000 in the week ending Nov. 20, the Labor Department said. The report raised hopes that more gains in hiring will be seen.

Still, another report showed that orders to U.S. factories for costly manufactured goods plunged in October by the largest amount in 21 months.

Durable-goods orders dropped 3.3 percent last month, the biggest setback since January 2009, when the country was still mired in a recession.

Of special concern was a 4.5 percent drop in orders for nondefense capital goods, excluding aircraft. This category is viewed as a good proxy for business investment plans. It was the biggest drop since a 5.3 percent fall in July.

Meanwhile, sales of new homes fell in October to near a record low and home prices dropped to the lowest point in seven years.

Sales of new single-family homes declined 8.1 percent to a seasonally adjusted annual rate of 283,000 units in October, Commerce said in another report. That was just 2.9 percent above the all-time low of 275,000 units hit in August for government records that go back to 1963.

The median price of a home sold in October dipped to $194,900, the lowest level since October 2003.

Even with the pickup in spending, consumers are still shying away from the type of buying needed to dramatically lower the 9.6 unemployment rate.

Normally after a recession, consumers spend more freely. But more than one year after the recession ended, Americans are more focused on getting their personal finances in order. They are paring down debt, watching their spending and building savings.

Americans saved 5.7 percent of their disposable income in October. That was up from 5.6 percent in September and was the most since August. Before the recession, they were saving just over 1 percent.

Federal Reserve Chairman Ben Bernanke and other economists worry that high unemployment, hard-to-get-credit, weak home values and lackluster wage growth are forces that will restrain the growth in consumer spending.

To counter that and try to invigorate the economy, the Fed recently launched a $600 billion program to buy government bonds. By doing so, the Fed hopes to boost stock prices and make loans cheaper, positive developments that could make people want to spend more.

Even faced with all the negative forces, Americans are still buying. That’s important because their spending accounts for roughly 70 percent of all economic output. With consumers holding up, fears the economy could slip back into a recession have receded.

In the July-September quarter, consumer spending grew at a 2.8 percent pace, the most in nearly four years.

Leading economists in an AP Economy Survey predict consumer spending will grow at a 2.4 percent pace in the October-December quarter. Consumer spending would need to grow by at least twice that pace to translate into the type of robust economic growth to make a big dent in the nation’s unemployment rate.

The nation’s unemployment rate has been stuck at 9.6 percent unemployment rate for the past three months. New projections from Federal Reserve suggest that won’t change much for a few years.

Copyright © 2010 The Associated Press, Jeannie Aversa, AP economics writer. AP Economics Writers Christopher Rugaber and Martin Crutsinger contributed to this report.

All told, the latest government data released the day before Thanksgiving suggest an improving picture of the economy. Income and spending are rising, and layoffs are slowing. This comes amid a decline in manufacturing activity, which had been a source of strength for months after the recession ended, and a struggling housing market.

Analysts question whether incomes can continue to grow at a consistent pace and keep consumers spending enough to invigorate the economy.

“The flurry of U.S. data this morning suggests that households have started to pickup the baton of growth from businesses,” said Paul Dales, U.S. economist at Capital Economics. “Whether or not households will be able to shoulder the burden of growth on their own is another matter.”

Investors appeared to be pleased by the data. The Dow Jones industrial average climbed more than 137 points in the early morning trading.

Consumers boosted their spending 0.4 percent in October, the Commerce Department said Wednesday. That was up from a 0.3 percent increase in September.

People showed a slightly bigger appetite to spend because their incomes rose 0.5 percent, reflecting a slowly healing jobs market that gave a boost to wages and salaries. Incomes didn’t grow at all in September. The increases in both income and spending last month were the most since August.

And inflation is running lower at a record low. Prices for goods excluding food and energy rose just 0.9 percent in the 12 months ending in October, the Commerce report noted. That was down from a 1.2 percent annual gain posted in September. Inflation is running at a pace below the Fed’s comfort zone of between 1.5 percent and 2 percent.

“We have a good signal,” John Silvia, chief economist at Wells Fargo, said of the jobless claims and consumer spending reports.

The pace of layoffs slowed to the lowest level since July 2008. Initial jobless claims dropped by 34,000 to a seasonally adjusted 407,000 in the week ending Nov. 20, the Labor Department said. The report raised hopes that more gains in hiring will be seen.

Still, another report showed that orders to U.S. factories for costly manufactured goods plunged in October by the largest amount in 21 months.

Durable-goods orders dropped 3.3 percent last month, the biggest setback since January 2009, when the country was still mired in a recession.

Of special concern was a 4.5 percent drop in orders for nondefense capital goods, excluding aircraft. This category is viewed as a good proxy for business investment plans. It was the biggest drop since a 5.3 percent fall in July.

Meanwhile, sales of new homes fell in October to near a record low and home prices dropped to the lowest point in seven years.

Sales of new single-family homes declined 8.1 percent to a seasonally adjusted annual rate of 283,000 units in October, Commerce said in another report. That was just 2.9 percent above the all-time low of 275,000 units hit in August for government records that go back to 1963.

The median price of a home sold in October dipped to $194,900, the lowest level since October 2003.

Even with the pickup in spending, consumers are still shying away from the type of buying needed to dramatically lower the 9.6 unemployment rate.

Normally after a recession, consumers spend more freely. But more than one year after the recession ended, Americans are more focused on getting their personal finances in order. They are paring down debt, watching their spending and building savings.

Americans saved 5.7 percent of their disposable income in October. That was up from 5.6 percent in September and was the most since August. Before the recession, they were saving just over 1 percent.

Federal Reserve Chairman Ben Bernanke and other economists worry that high unemployment, hard-to-get-credit, weak home values and lackluster wage growth are forces that will restrain the growth in consumer spending.

To counter that and try to invigorate the economy, the Fed recently launched a $600 billion program to buy government bonds. By doing so, the Fed hopes to boost stock prices and make loans cheaper, positive developments that could make people want to spend more.

Even faced with all the negative forces, Americans are still buying. That’s important because their spending accounts for roughly 70 percent of all economic output. With consumers holding up, fears the economy could slip back into a recession have receded.

In the July-September quarter, consumer spending grew at a 2.8 percent pace, the most in nearly four years.

Leading economists in an AP Economy Survey predict consumer spending will grow at a 2.4 percent pace in the October-December quarter. Consumer spending would need to grow by at least twice that pace to translate into the type of robust economic growth to make a big dent in the nation’s unemployment rate.

The nation’s unemployment rate has been stuck at 9.6 percent unemployment rate for the past three months. New projections from Federal Reserve suggest that won’t change much for a few years.

Copyright © 2010 The Associated Press, Jeannie Aversa, AP economics writer. AP Economics Writers Christopher Rugaber and Martin Crutsinger contributed to this report.

Thursday, November 18, 2010

NOW IS THE TIME TO BUY!

MORTGAGE RATES JUMPED TO 4.39% FOR A 30 YEAR FIXED LOAN

Courtesy of the Wall Street Journal, November 18, 2010

Home-mortgage rates rose in the latest week, with most of the rates that Freddie Mac follows bouncing off of all-time lows and the 30-year rate rising to 4.39%, according to Freddie's weekly survey of mortgage rates.

Rates have slumped for months, setting record lows in the process, as yields on Treasurys slid amid economic uncertainty. But yields jumped sharply the past week. Mortgage rates generally track the yields, which move inversely to Treasury prices.

The 30-year fixed-rate mortgage averaged 4.39% for the week ended Thursday, up from the prior week's 4.17% average but down from 4.83% a year ago. The latest figure was a three-month high.

Rates on 15-year fixed-rate mortgages were 3.76%, up from 3.57% the previous week but down from 4.32% a year earlier.

Both of the fixed-rate loans had set record-low averages a week earlier.

Five-year Treasury-indexed hybrid adjustable-rate mortgages averaged 3.4%, up from the prior week's 3.25% but down from 4.25% a year earlier. One-year Treasury-indexed ARMs were 3.26%, flat with the prior week and down from 4.35% a year earlier.

To obtain the rates, the 30-year fixed-rate mortgages required payment of an average 0.9 point, the 15- and five-years required an average 0.7 point and the one-year required a 0.6. A point is 1% of the mortgage amount, charged as prepaid interest.

Write to Nathan Becker with the Wall Street Journal at nathan.becker@dowjones.com

Courtesy of the Wall Street Journal, November 18, 2010

Home-mortgage rates rose in the latest week, with most of the rates that Freddie Mac follows bouncing off of all-time lows and the 30-year rate rising to 4.39%, according to Freddie's weekly survey of mortgage rates.

Rates have slumped for months, setting record lows in the process, as yields on Treasurys slid amid economic uncertainty. But yields jumped sharply the past week. Mortgage rates generally track the yields, which move inversely to Treasury prices.

The 30-year fixed-rate mortgage averaged 4.39% for the week ended Thursday, up from the prior week's 4.17% average but down from 4.83% a year ago. The latest figure was a three-month high.

Rates on 15-year fixed-rate mortgages were 3.76%, up from 3.57% the previous week but down from 4.32% a year earlier.

Both of the fixed-rate loans had set record-low averages a week earlier.

Five-year Treasury-indexed hybrid adjustable-rate mortgages averaged 3.4%, up from the prior week's 3.25% but down from 4.25% a year earlier. One-year Treasury-indexed ARMs were 3.26%, flat with the prior week and down from 4.35% a year earlier.

To obtain the rates, the 30-year fixed-rate mortgages required payment of an average 0.9 point, the 15- and five-years required an average 0.7 point and the one-year required a 0.6. A point is 1% of the mortgage amount, charged as prepaid interest.

Write to Nathan Becker with the Wall Street Journal at nathan.becker@dowjones.com

CHECK OUT OUR NEW AND REDUCED LISTINGS AT www.HughesShelton.com

Thursday, October 28, 2010

Mortgage Rates at an All Time Low

Mortgage rates hit decades-low 4.19%

WASHINGTON – Oct. 15, 2010 – Rates on 30-year mortgages fell this week to 4.19 percent, the lowest level in decades. They were pushed down by lower Treasury bond yields.

Investors are buying up Treasury bonds in anticipation of a move by the Federal Reserve designed to lower mortgage rates and yields on corporate debt.

As a result, the average rate for 30-year fixed loans dropped to the lowest level on records dating back to 1971, mortgage buyer Freddie Mac said Thursday. It’s down from 4.27 percent the previous week. The last time rates were this low was in the early 1950s.

The average rate on 15-year fixed loans fell to 3.62 percent, the lowest on records dating back to 1991, Freddie Mac said.

Rates have fallen since spring as investors shifted money into the safety of Treasury bonds. That demand lowers their yields, which mortgage rates tend to track. The 30-year rate was 5.08 percent at the beginning of April. The 15-year rate was 4.39 percent.

Low rates haven’t helped the struggling housing market, which recorded its worst summer in more than a decade. But they have led to a surge in refinancing.

And rates could fall even further in the coming week.

The Federal Reserve is leaning toward buying more Treasury bonds to drive down loan rates and boost the economy, according to minutes of closed-door deliberations released Tuesday. Economists predict Fed officials will approve a bond purchase program at their Nov. 2-3 meeting.

Two Fed officials in recent remarks have suggested the new purchases shouldn’t exceed $500 billion. That would be smaller than a $1.7 trillion program launched during the recession.

The program would likely push mortgage rates down – possibly lower than 4.0 percent on the 30-year fixed loan.

Some analysts say rates are more likely to hover above 4.0 percent, without breaking that threshold.

"A lot of the impact that you would expect from this program is already priced into the market," said Mike Larson, real estate and interest rate analyst at Weiss Research. "If there’s any risk, it’s that what the Fed announces turns out to be a disappointment in some way. You might see rates go up a little bit."

To calculate average mortgage rates, Freddie Mac collects rates from lenders around the country on Monday through Wednesday of each week. Rates often fluctuate significantly, even within a given day.

Rates on five-year adjustable-rate mortgages averaged 3.47 percent, the same as the previous week. Rates on one-year adjustable-rate mortgages rose to an average of 3.43 percent from 3.4 percent.

The rates do not include add-on fees known as points. One point is equal to 1 percent of the total loan amount. The nationwide fee for loans in Freddie Mac’s survey averaged 0.8 a point for 30-year and 1-year mortgages. It averaged 0.7 of a point for 15-year and 0.6 of a point for 5-year mortgages.

Copyright © 2010 Associated Press. All rights reserved.

Investors are buying up Treasury bonds in anticipation of a move by the Federal Reserve designed to lower mortgage rates and yields on corporate debt.

As a result, the average rate for 30-year fixed loans dropped to the lowest level on records dating back to 1971, mortgage buyer Freddie Mac said Thursday. It’s down from 4.27 percent the previous week. The last time rates were this low was in the early 1950s.

The average rate on 15-year fixed loans fell to 3.62 percent, the lowest on records dating back to 1991, Freddie Mac said.

Rates have fallen since spring as investors shifted money into the safety of Treasury bonds. That demand lowers their yields, which mortgage rates tend to track. The 30-year rate was 5.08 percent at the beginning of April. The 15-year rate was 4.39 percent.

Low rates haven’t helped the struggling housing market, which recorded its worst summer in more than a decade. But they have led to a surge in refinancing.

And rates could fall even further in the coming week.

The Federal Reserve is leaning toward buying more Treasury bonds to drive down loan rates and boost the economy, according to minutes of closed-door deliberations released Tuesday. Economists predict Fed officials will approve a bond purchase program at their Nov. 2-3 meeting.

Two Fed officials in recent remarks have suggested the new purchases shouldn’t exceed $500 billion. That would be smaller than a $1.7 trillion program launched during the recession.

The program would likely push mortgage rates down – possibly lower than 4.0 percent on the 30-year fixed loan.

Some analysts say rates are more likely to hover above 4.0 percent, without breaking that threshold.

"A lot of the impact that you would expect from this program is already priced into the market," said Mike Larson, real estate and interest rate analyst at Weiss Research. "If there’s any risk, it’s that what the Fed announces turns out to be a disappointment in some way. You might see rates go up a little bit."

To calculate average mortgage rates, Freddie Mac collects rates from lenders around the country on Monday through Wednesday of each week. Rates often fluctuate significantly, even within a given day.

Rates on five-year adjustable-rate mortgages averaged 3.47 percent, the same as the previous week. Rates on one-year adjustable-rate mortgages rose to an average of 3.43 percent from 3.4 percent.

The rates do not include add-on fees known as points. One point is equal to 1 percent of the total loan amount. The nationwide fee for loans in Freddie Mac’s survey averaged 0.8 a point for 30-year and 1-year mortgages. It averaged 0.7 of a point for 15-year and 0.6 of a point for 5-year mortgages.

Copyright © 2010 Associated Press. All rights reserved.

Monday, October 18, 2010

Price Reduction

4210 Gray St, #3 has recently been reduced to $239,900! This immaculate three bedroom, 3 bath townhome is conveniently located with easy access to all bridges, shopping, movies, dining and airport. Features include; a spacious floor plan with wood floors, bright kitchen with granite counter-tops, private patio, first floor guest suite and attached one car garage. No maintenance fees.

Check out our website for more information and our other listings: http://www.hughesshelton.com/

Check out our website for more information and our other listings: http://www.hughesshelton.com/

Tuesday, October 5, 2010

Florida's Exisiting Home and Condo Sales up in August

Sales of existing homes in Florida rose 1 percent in August compared to homes sold in August 2009, according to the latest housing data released by Florida Realtors®. Statewide existing home sales in August increased 3 percent over statewide sales activity in July and Florida’s condo sales increased 22 percent since August 2009. Statewide existing condo sales last month increased almost 2.7 percent over July’s condo sales.

For more information on this story, click here: http://ow.ly/198cio

For more information on this story, click here: http://ow.ly/198cio

Saturday, October 2, 2010

Waterfront Price Reduction

Great price reducation on Waterfront home in ideal Beach Park Location.

4816 Beachway is now listed at $2,195,000.00!

The property is also being offered for lease at $7,000.00.

See all of our listings at http://www.hughesshelton.com/.

Wednesday, August 25, 2010

Largest Home Sale in Tampa

Coldwell Banker is pleased to report that Andrea Rottensteiner with Hughes-Shelton Realtors recently closed the largest single family home sale since 2008 in Hillsborough County totaling 9.2 million dollars. The buyer's names were not disclosed at the time of the closing.

The buyer purchased a $6 million home in South Tampa on the beautiful Palma Ceia Golf Course. In addition to this home for he also purchased the home next door for $3.2 million.

The main home is located at 914 S. Golf View and was built in 2006. The home features 5 bedrooms, 5.5 baths with 8,351 square feet. Special features include: French Limestone throughout; outdoor kitchen with custom hood, viking gas grill, bar, custom wine cellar, Butler’s Pantry, central audio/visual system, power draperies & shades, custom cabinetry throughout, his and her Study, and an air conditioned 3+ Car Garage with storage and utility room.

The smaller home, at 910 Golf View, has 3,244 square feet and 5 bedrooms and 2 baths. It was built in 1939 and last sold for $1.2 million in 2008.

Hughes-Shelton Realtors of Coldwell Banker Residential Real Estate has helped families open new doors to their future for more than 25 years. Specializing in buying, selling and renting distinguished properties for an exceptional client base, Hughes-Shelton Realtors understand that real estate is much more than a financial transaction. It’s an important, well-earned life change.

With the highest standard of excellence in service and meticulous attention to details, Hughes-Shelton Realtors have earned a reputation as one of Tampa’s top real estate teams. Mike Hughes and Jeff Shelton’s philosophy is ‘to give real service, you must add something which cannot be bought or measured with money, and that is sincerity and integrity’.

The buyer purchased a $6 million home in South Tampa on the beautiful Palma Ceia Golf Course. In addition to this home for he also purchased the home next door for $3.2 million.

The main home is located at 914 S. Golf View and was built in 2006. The home features 5 bedrooms, 5.5 baths with 8,351 square feet. Special features include: French Limestone throughout; outdoor kitchen with custom hood, viking gas grill, bar, custom wine cellar, Butler’s Pantry, central audio/visual system, power draperies & shades, custom cabinetry throughout, his and her Study, and an air conditioned 3+ Car Garage with storage and utility room.

The smaller home, at 910 Golf View, has 3,244 square feet and 5 bedrooms and 2 baths. It was built in 1939 and last sold for $1.2 million in 2008.

Hughes-Shelton Realtors of Coldwell Banker Residential Real Estate has helped families open new doors to their future for more than 25 years. Specializing in buying, selling and renting distinguished properties for an exceptional client base, Hughes-Shelton Realtors understand that real estate is much more than a financial transaction. It’s an important, well-earned life change.

With the highest standard of excellence in service and meticulous attention to details, Hughes-Shelton Realtors have earned a reputation as one of Tampa’s top real estate teams. Mike Hughes and Jeff Shelton’s philosophy is ‘to give real service, you must add something which cannot be bought or measured with money, and that is sincerity and integrity’.

Subscribe to:

Posts (Atom)